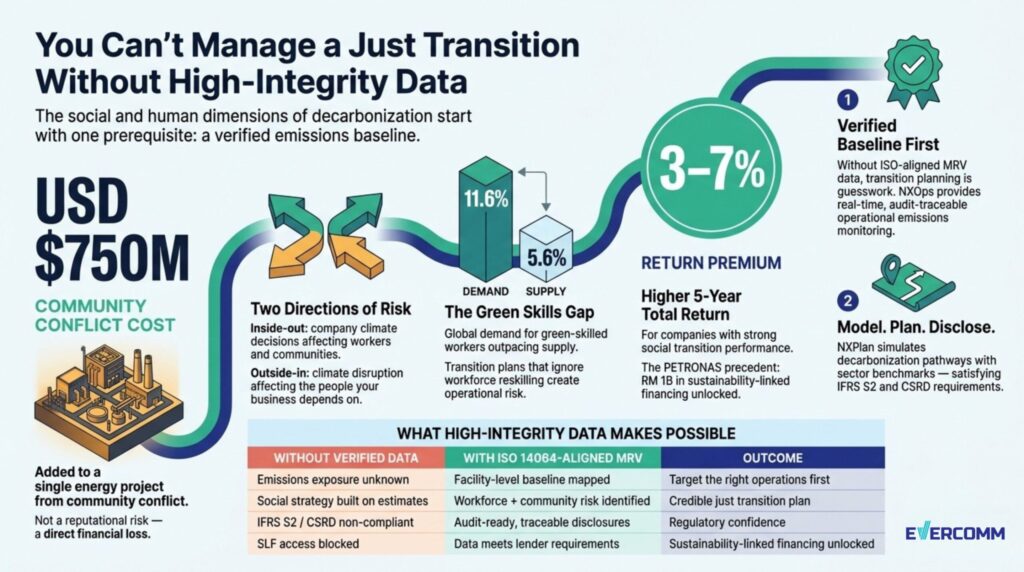

A single energy project in the Asia-Pacific region faced USD $750 million in added costs because of community conflict. Not regulatory fines. Not carbon taxes. Community conflict — the kind that builds when workers and local populations feel they have been excluded from decisions that will reshape their livelihoods.

That number comes from research compiled by the

World Business Council for Sustainable Development and ERM. It is not an outlier. It is a signal that the social dimensions of corporate decarbonization — worker displacement, supply chain pressure, community trust — carry real financial weight. And the companies that treat them as secondary considerations are learning that lesson at scale.

But here is the part that rarely gets discussed: almost every framework for managing the social dimensions of transition begins with the same prerequisite. You need to know exactly where your emissions stand today. Not roughly. Not across your industry benchmark. Your operations, your baseline, your verified numbers.

Without that, there is nothing to build a transition plan on.

The Just Transition Is a Business Problem, Not a Values Exercise

The term “just transition” has roots in labour rights advocacy, but its current relevance to CFOs and operations directors has nothing to do with idealism. It has to do with material risk.

The WBCSD/ERM framework describes just transition as having two active dimensions. The first is inside-out: the direct impact of your company’s climate decisions on your workers, your suppliers, and the communities where you operate. Which roles disappear when a facility decarbonizes? Which suppliers lose contracts when you shift away from carbon-intensive inputs? What happens to a town when the plant that employs 20% of its workforce changes production methods?

The second is outside-in: the ways in which physical climate disruption affects the people your business depends on. Workforce skills gaps. Community instability. Supply chain fragility. The green skills shortage is already measurable — global demand for green-skilled workers rose 11.6% in 2023–2024, while supply only grew 5.6%. If your transition plan doesn’t account for reskilling, you are building operational risk into your own roadmap.

The financial case is well-established. Companies with strong social performance deliver 3–7% higher five-year total return. PETRONAS Malaysia unlocked RM 1 billion — approximately USD $230 million — in sustainability-linked financing by building supplier ESG readiness. The data-backed transition plan was not a compliance cost. It was a financing instrument.

CFOs now carry specific accountability here. Incorporating social risks into financial disclosures, transition cost planning, green finance readiness — these sit explicitly in the CFO’s mandate under emerging frameworks including IFRS S2 and the EU’s CSRD. The C-suite distribution of responsibility is shifting. The CFO is no longer adjacent to transition planning. They are at the centre of it.

The Most Common Mistake: Building Strategy on Unverified Data

Most companies approaching just transition planning start with the social side: stakeholder engagement plans, workforce impact assessments, community consultation processes. That work is necessary. But it is being built, in most cases, on an emissions baseline that has never been independently verified.

The consequences are not theoretical. Without a verified emissions baseline, you cannot reliably identify which operations drive the greatest exposure for workers and communities — because you do not know which parts of your business are driving the most carbon. You cannot model credible reduction scenarios, because your starting point is uncertain. You cannot satisfy IFRS S2 or CSRD transition plan requirements, because those frameworks explicitly require measurable, traceable data. And you cannot access sustainability-linked financing, because lenders are no longer accepting self-reported figures as sufficient.

The TPT transition planning cycle — Re-assess, Set ambition, Plan actions, Implement — is the vehicle through which people-centred considerations get embedded in corporate decarbonization. But that cycle starts with Re-assess. And Re-assess means credible baseline data.

A just transition plan built on incomplete, unaudited, or inconsistently measured emissions data is not a transition plan. It is a narrative. It may satisfy internal stakeholders for a while. It will not satisfy a Bureau Veritas audit, an IFRS S2 disclosure review, or the community relations team when promised outcomes do not materialise.

The social strategy sits on top of the data layer. The data layer has to be sound.

What Leading Companies Are Doing Differently

The industrial companies getting this right are not necessarily the ones with the most sophisticated sustainability teams. They are the ones that established measurement discipline early and built everything else on top of it.

In practical terms, that means: real-time operational emissions monitoring that captures facility-level data continuously, not just at annual reporting intervals. It means ISO 14064-aligned measurement so that the data is structured the same way it will need to be structured for any independent verification or regulatory submission. It means audit trails — traceable data that can be interrogated, not just reported.

With that foundation in place, something useful becomes possible. You can map your emissions geography to your workforce geography. You can identify which facilities are highest-emitting and therefore most likely to be subject to transformation pressure — and plan workforce and community interventions accordingly, with lead time. You can model different decarbonization scenarios and understand the differential social impact of each pathway before you commit to one.

This is what it means to manage a just transition with precision rather than aspiration.