Beyond the Alphabet Soup:

Why Governance and Risk Management Are the New ESG Standard in 2026

Date

23/03/2026

Category

General

Share

Linkedin-in

Jki-whatsapp-1-light

Jki-message-1-light

ESG is no longer a marketing exercise; it is a matter of ESG governance and risk management.

If you have ever looked at the landscape of sustainability reporting and felt overwhelmed, you are not alone.

As Pooja Premjyothi Sanjayan recently noted in a thought-provoking LinkedIn post, the “alphabet soup” of ESG frameworks — from GRI to ISSB to CSRD — can feel impenetrable.

However, as we move through 2026, the conversation is shifting. We are moving away from simply memorizing acronyms and toward a fundamental operational reality:

For organizations today, untangling the complexity starts with understanding why these frameworks exist. They are designed to measure and manage sustainability performance in a structured, transparent way — going beyond financial returns to address long-term risks.

Here is what the latest research says about the state of ESG in 2026, and how businesses can navigate it..

1. The “G” Is the Enabler of “E” and “S”

For years, the Environmental pillar of ESG took center stage. In 2026, Governance has emerged as the linchpin that makes sustainability credible.

Governance is now the enabler that ensures environmental and social goals are achieved responsibly.

From Compliance to Strategy

Corporate governance has moved beyond compliance checklists to become a benchmark for resilience. Boards are shifting from passive oversight to active, data-driven governance.

The Accountability Shift

Boards are increasingly being held accountable for sustainability performance.

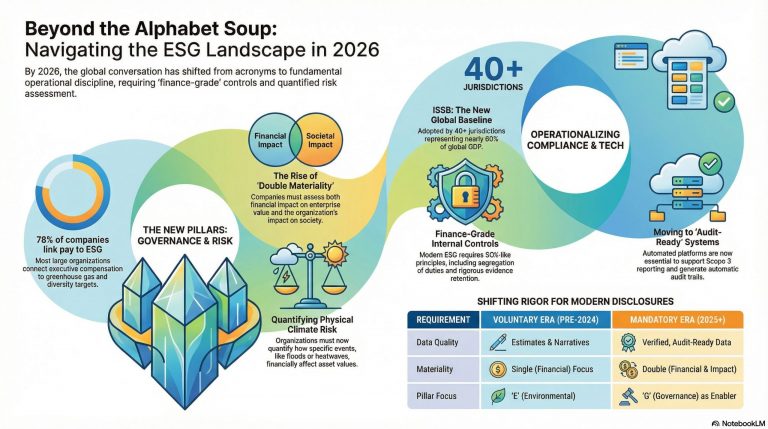

- 78% of large companies now link executive compensation to sustainability targets

The most common metrics relate to:

- Greenhouse gas (GHG) emissions

- Workforce diversity

Internal Controls Go “Finance-Grade”

Modern ESG programs now require the same rigor as financial reporting.

- Appointment of ESG Controllers

- Alignment with SOX-like principles, including:

- Segregation of duties

- Strong documentation

- Evidence retention

2. Risk Management: Quantifying the Financial Impact

The days of vague, narrative-driven climate risk statements are over.

In 2026, regulations such as California’s SB 261 and the IFRS S2 standard require companies to treat climate risk as a financial risk, reinforcing the role of ESG governance and risk management at the board level.

Financial vs. Impact Materiality

The concept of Double Materiality is reshaping reporting, particularly for companies with EU exposure.

Organizations must assess:

- Financial Materiality — how sustainability issues affect enterprise value

- Impact Materiality — how the organization affects society and the environment

Quantifying Physical Risks

It is no longer sufficient to state exposure to climate risks. Companies must quantify how specific risks — such as floods or heatwaves — affect asset values and operational continuity.

Supply Chain Vulnerability

Risk management now extends deep into the value chain.

With Scope 3 emissions reporting becoming mandatory in jurisdictions such as California (by 2027) and the EU, companies must manage sustainability data across thousands of suppliers.

3. Untangling the Frameworks: Convergence and Divergence

While the “alphabet soup” persists, 2026 has brought meaningful consolidation and clarity to the global reporting landscape.

The Global Baseline: ISSB

The ISSB standards (IFRS S1 and S2) are emerging as the global baseline.

- Adopted by over 40 jurisdictions

- Representing nearly 60% of global GDP

- Integrating TCFD and SASB into a single, coherent framework

The European Standard: CSRD

The EU’s CSRD remains the most comprehensive mandate globally.

Recent “Omnibus” simplification measures:

- Raise reporting thresholds

- Reduce burden on smaller companies

- Maintain rigor for large enterprises

The US Landscape

Despite delays at the federal level, state-level regulations — particularly California’s SB 253 and SB 261 — have effectively created nationwide disclosure expectations for large US companies.

4. The Role of Technology: Moving to “Audit-Ready”

As ESG disclosures shift from voluntary to mandatory, operational expectations have changed dramatically.

Voluntary reports could rely on estimates. Mandatory disclosures require audit trails, controls, and assurance — turning ESG governance and risk management into a systems and data challenge, not just a reporting one. (Keyword use #3)

Automated Data Collection

Manual spreadsheets cannot support double materiality analysis or large-scale Scope 3 data. Automated platforms are now essential.

Audit-Readiness by Design

Effective systems must:

- Generate audit trails automatically

- Log data sources and approvals

- Support limited and reasonable assurance

Turning ESG Data into Strategic Advantage

Navigating ESG in 2026 requires looking beyond acronyms and focusing on fundamentals: governance discipline and risk rigor.

Organizations that treat sustainability data with the same standards as financial data can transform compliance into a strategic advantage — strengthening resilience, meeting investor expectations, and supporting long-term value creation.

At Evercomm, we help businesses bridge the gap between complex frameworks and operational reality. Our NXMap and NXOps solutions deliver precision-driven, audit-ready data to help organizations navigate the 2026 regulatory landscape with confidence.

Browse More Articles

Just Transition Planning Needs High-Integrity Emissions Data

Companies building just transition strategies on unverified carbon data face real financial and regulatory…

ISO 14001:2026 Update: What Changed and What It Means

ISO 14001:2026 published April 2026. Understand the key changes from 2015, what’s now required, and how…

ESG Reporting Was Never Just Compliance. It Wins Contracts, Better Financing, and Trust.

Most companies treat ESG reporting as a compliance task. Here’s what it actually unlocks — contracts,…