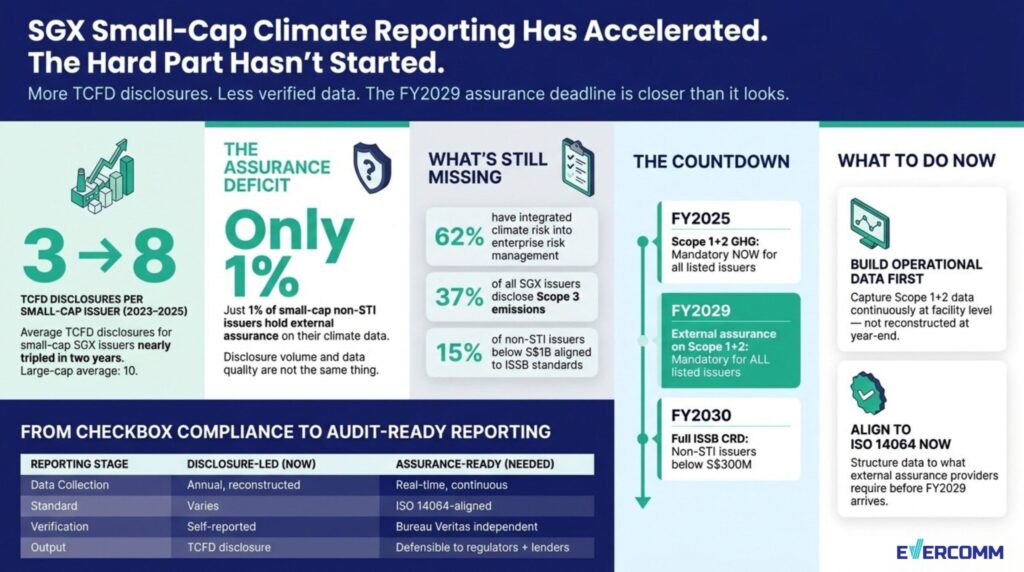

Two years ago, the average small-cap company on SGX published three TCFD disclosures. Today that number is eight — nearly matching the large-cap average of ten. Singapore’s smaller listed companies have nearly closed the gap on their larger peers in SGX climate reporting.

That is genuinely impressive progress. And it is almost entirely beside the point.

Because the metric that actually matters — the percentage of small-cap non-STI issuers with external assurance on their climate data — sits at 1%. Not 1% growth. 1% total. External limited assurance on Scope 1 and 2 emissions becomes mandatory for all listed issuers from FY2029. That number defines the real state of readiness.

The disclosures are multiplying. The infrastructure behind them is not.

What the Numbers Actually Show

The SGX and NUS CGS Sustainability Reporting Review 2025 reviewed 499 listed issuers, providing the most comprehensive picture of SGX climate reporting readiness available. Its headline findings are worth taking seriously. Ninety-nine percent of those issuers provided at least one TCFD disclosure — a figure that would have been unthinkable five years ago. The Strategy pillar, historically the weakest area of TCFD compliance, jumped from 78% to 92% in a single year. And 62% of small-cap issuers now report between 8 and 11 disclosures.

These numbers reflect real effort. Finance teams at small manufacturers and industrials across Singapore have been building sustainability reporting capacity under genuine resource constraints. SGX RegCo acknowledged in 2025 that “the standards are ambitious and that smaller companies, in particular, have found compliance challenging” — and adjusted the deadlines accordingly. Non-STI issuers below S$300 million market cap now have until FY2030 for full ISSB Climate-related Disclosures compliance. Scope 3 reporting remains voluntary for this group for now.

The deadline extension is a practical concession. It is not a signal that the destination has changed.

The SGX Climate Reporting Gap the Headlines Are Masking

More TCFD boxes ticked does not mean more reliable climate data. And the gap between the two is where the real exposure sits.

Only 62% of SGX-listed issuers have formally integrated climate risk into their enterprise risk management processes. For more than a third of listed companies, climate risk is disclosed in a sustainability report but not tracked through the frameworks governing other material business risks. The disclosure exists. The management process does not.

Scope 3 reporting tells a similar story. Thirty-seven percent of all SGX-listed issuers disclose Scope 3 emissions — 31% for small non-STI issuers. Research from Schneider Electric and ISCA puts it more bluntly: 90% of Singapore companies are not fully measuring or analysing their Scope 3 emissions at all.

The ISSB adoption figures complete the picture. Sixty-three percent of STI constituents are aligned to ISSB. For non-STI issuers below S$1 billion, that drops to 15%. Only 4% of small and mid-cap companies told the Singapore Business Federation in June 2025 that they felt strong confidence in meeting earlier compliance deadlines.

The gap is not between intention and effort. It is between the volume of disclosures and the quality of the underlying data.

Kok Ping Soon, CEO of the Singapore Business Federation, put it plainly: “Small- and mid-cap listed companies have started preparing, though many continue to face practical barriers — including incomplete understanding of disclosure requirements and a lack of time and resources.”

The Deadlines That Change the Calculation

The August 2025 timeline revisions gave smaller companies more runway on full ISSB alignment. But they did not move the Scope 1 and 2 GHG reporting requirement — that applies to all listed issuers from FY2025. And external limited assurance on Scope 1 and 2 data is mandatory for all listed issuers from FY2029.

That four-year window sounds comfortable. It is not, for two reasons.

First, assurance-grade reporting is not a switch you flip in year three. Building the data collection processes, measurement systems, and audit trails that external assurance requires takes time — typically two to three years before a first audit is credible. Companies that start in 2027 will be racing.

Second, the barriers are structural. A Schneider Electric and SGX survey of 543 companies identified the top four compliance challenges as: internal skills gaps (55%), high costs (52%), data gaps (43%), and insufficient external provider support (42%). None of those are solved by writing better disclosures. They are solved by building measurement infrastructure first.

FY2030 is not a finish line. It is the point at which the infrastructure needs to be operational.