Every regulator in APAC is saying the same thing — just in different languages

In June 2026,

China’s National Financial Regulatory Administration began rolling out Yi Biao Tong, a unified reporting system designed to replace fragmented, form-based submissions with transaction-level granular data. Across the region, Hong Kong, Malaysia, Thailand, India, Australia, and Japan are each pursuing the same objective: retiring aggregated reports in favour of element-level, machine-readable submissions that regulators can query directly.

This is not a coincidence. It is a structural shift. And the granular data mandate driving it extends well beyond prudential and financial reporting.

The same demand for transaction-level, asset-specific, verifiable data is now embedded in climate disclosure frameworks — IFRS S2, MAS climate risk guidelines, and the latest PCAF methodology. Banks that recognise the overlap early will build one infrastructure layer. Banks that do not will build two, maintain both, and still struggle with data quality in each.

The APAC regulatory reset: a region moving in lockstep

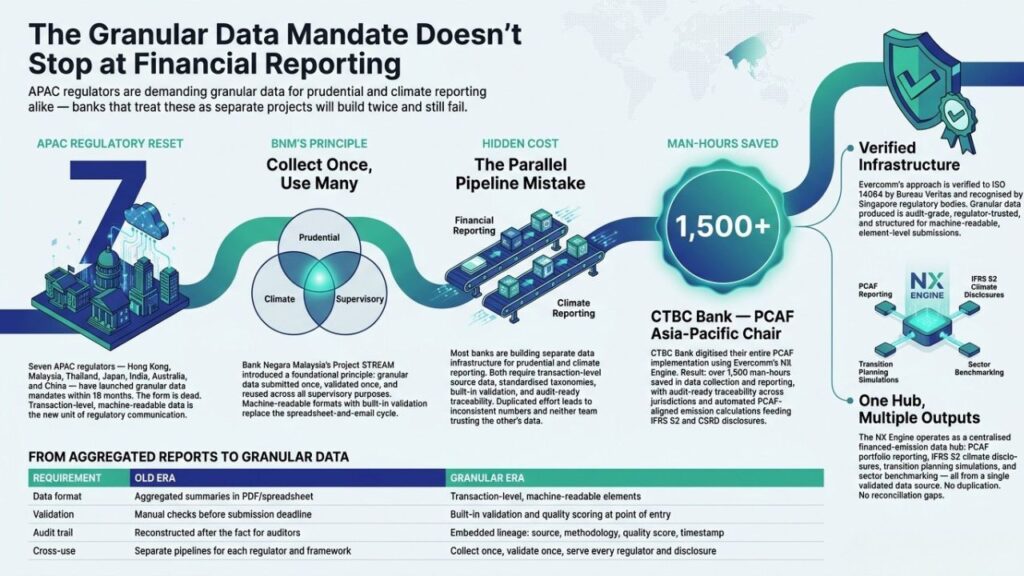

The pace is striking. Within a span of 18 months, nearly every major APAC regulator has announced or launched a granular data reporting initiative.

Hong Kong’s GDR 3.0 is the most closely watched. The Hong Kong Monetary Authority co-designed the framework with the banking industry, establishing an official data dictionary and phased rollout through 2028. Banks are accountable for the accuracy of every data element they submit — not just the summary figures.

Malaysia’s Project STREAM, led by Bank Negara Malaysia, introduced a principle that deserves attention far beyond Kuala Lumpur: “Collect Once, Use Many.” Rather than asking banks to fill multiple forms with overlapping data, BNM is building a system where granular data is submitted once and reused across supervisory purposes. Machine-readable formats with built-in validation replace the old spreadsheet-and-email cycle.

Thailand’s RDT Phase 2 follows a similar logic. The Bank of Thailand is replacing form-based reports with entity-level and data-element-level submissions — moving from asking “what does this report say?” to “what does the underlying data show?”

Japan has already begun full-scale granular data collection from the Bank of Japan as of March 2025.

India’s RBI is shifting to element-based reporting.

Australia’s APRA is moving toward data-driven supervisory analysis. And China’s Yi Biao Tong, now in its initial rollout phase through December 2027, aims to unify reporting across banking, insurance, and securities under one granular data architecture.

The common thread is unmistakable. Every regulator listed above has concluded that aggregated, form-based reports no longer provide the supervisory visibility they need. The replacement is universally the same: raw, transaction-level, machine-validated granular data that regulators can slice, query, and analyse on their own terms. Whether the label is GDR, STREAM, RDT, or Yi Biao Tong, the architectural blueprint is converging.

The direction is unanimous. The question for banks is not whether granular data will be required, but whether their infrastructure can serve more than one master.

The mistake: treating climate data as a separate problem

Here is where most banks are making a costly error.

Financial reporting teams are investing in granular data infrastructure to meet GDR 3.0, Project STREAM, or RDT Phase 2. Meanwhile, sustainability teams — often in a different building, reporting to a different executive — are building their own infrastructure to meet IFRS S2 disclosure requirements, MAS climate risk guidelines, and PCAF financed emissions calculations.

The two workstreams share almost identical underlying requirements:

– Transaction-level source data, not aggregated summaries

– Standardised taxonomies and data dictionaries

– Built-in validation and quality scoring at the point of submission

– Audit-ready traceability — every number must be defensible to a regulator or verifier

– Machine-readable outputs that integrate with downstream analytics

The overlap is not partial. It is structural. A bank’s loan-level exposure data feeds both its prudential reporting and its Scope 3 Category 15 financed emissions calculations. The asset-level energy consumption data that supports IFRS S2 climate disclosures is the same data that informs credit risk models under Basel ESG requirements.

Yet most banks are building parallel pipelines — separate extraction, separate transformation, separate validation, separate storage. The result: duplicated effort, inconsistent numbers, and neither team confident in the other’s data.

BNM’s “Collect Once, Use Many” principle was designed precisely to prevent this. But the principle applies just as forcefully to climate and emissions data as it does to prudential reporting. Granular data collected at the asset level, validated once against a common standard, and served to multiple downstream consumers — financial, supervisory, and climate — is not just more efficient. It is more accurate.